We are loved because we keep our customers first and treat their needs with utmost importance.

7,40,000

APP DOWNLOADS

609

BRANCHES

₹10,714

Cr AUM

A1+

ICRA

AA+(STABLE)

INDIA RATINGS

AA+(Stable)

CARE

AA(positive) / A1+

CRISIL

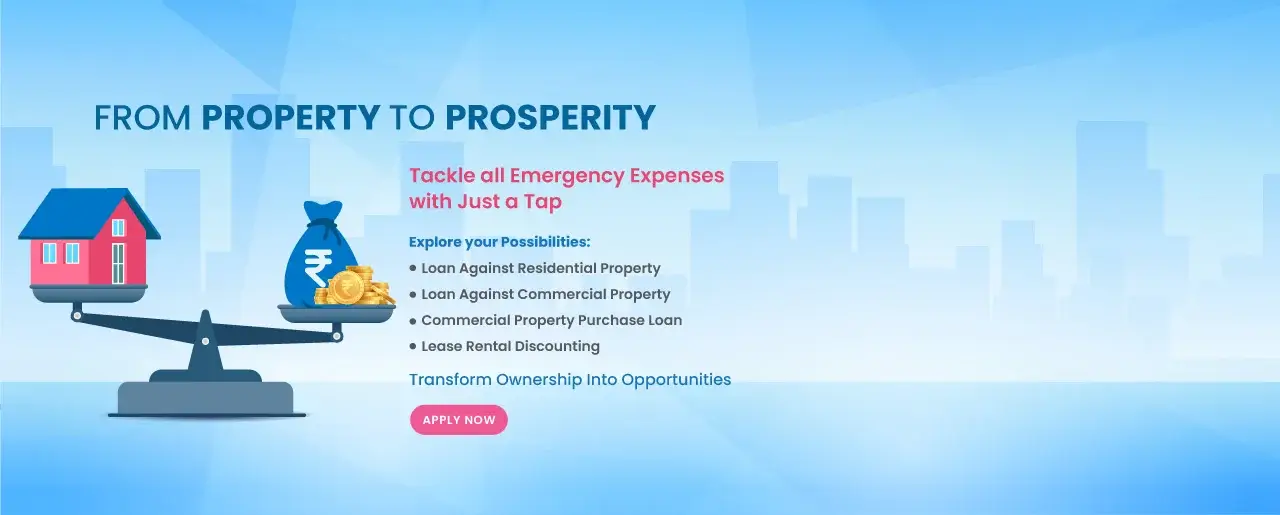

Privilege Loan

3k

Min Loan Amount

Balance Transfer

![]()

3k

Min Loan Amount

Small Ticket Loan

1 Lac

Min Loan Amount

High Value Loan

5 Lac

Min Loan Amount

Loan Against Property customer, Andhra - Telangana State

Loan Against Property customer, Andhra - Telangana State

Loan Against Property customer, Andhra - Telangana State

Loan Against Property customer, Andhra - Telangana State

Loan Against Property customer, Andhra - Telangana State

Loan Against Property customer, Mumbai

Gold Loan customer, Channapatna Branch

Loan Against Property customer, Andhra- Telangana State

LAP customer, Mumbai

Gold Loan, Pune Branch

LAP customer, Mumbai

Gold Loan

Login

Login SMA/NPA Awareness

SMA/NPA Awareness Calculators

Calculators Quick Pay

Quick Pay Branch Locator

Branch Locator Support

Support About Us

About Us Work Spirit at Fedbank

Work Spirit at Fedbank Partner with us

Partner with us Employee Login

Employee Login Restart with Fedfina

Restart with Fedfina Awards & Accolades

Awards & Accolades